Polish Investment Zone

After over 20 years of the functioning of Special Economic Zones (SEZ), the Act of the 10th May 2018 on the support for new investments (Journal of Laws of 2023, item 74, as amended) introduced changes to the tax exemption instrument (CIT or PIT) in order to adapt the provisions to the current market situation and the needs of entrepreneurs. The amendment allows for tax exemption throughout Poland by companies implementing new investments, both on public and private sites, with the exception of sites where mineral deposits occur (unless the investment concerns such deposits). At the same time, existing permits for conducting economic activity in Special Economic Zones, remain valid until the end of 2026. Additionally, the amendment of 31 July 2019 allows support for investments in areas with untapped mineral deposits, thus significantly expanding the range of locations where entrepreneurs can receive tax exemptions. On 1 January 2022, an amendment to the Act came into force, which was largely related to the change in the regional aid map.

Special Economic Zones (SEZ) in Poland

A map of Poland with the areas administrated by Special Economic Zones separated

Write the name of the Powiat or town with Powiat legal status in which you wish to do business and we will direct your enquiry to the dedicated zone.

Select the Zone you are interested in from the list below or check the affiliation of Zones by province here.

SEZ Kamienna Góra

SEZ Katowice

SEZ Kostrzyn-Słubice

SEZ Kraków

SEZ Legnica

SEZ Łódź

SEZ Mielec

SEZ Pomorska

SEZ Słupsk

SEZ Starachowice

SEZ Suwałki

SEZ Tarnobrzeg

SEZ Wałbrzych

SEZ Warmińsko-Mazurska

Q&A / Frequently Asked Questions

What projects are eligible for support?

In the light of the provisions on regional state aid, the definition of a new investment reads as follows:

- setting-up of a new establishment

- extension of the capacity of an existing establishment

- diversification of the output of an establishment into products not previously produced in the establishment

- fundamental change in the overall production process of an existing establishment

- the acquisition of assets belonging to an establishment that has closed or would have closed had it not been purchased, and is bought by an investor unrelated to the seller

If the case of an investment by a large entrepreneur in the territory of the Dolnośląskie and Wielkopolskie Voivodship or Warsaw-Capital Region only an investment in favour of a new economic activity shall be considered a new investment.

As in the case of SEZs, investments implemented within certain sectors of economic activity will not be covered by the support system. A detailed catalogue of exemptions is set out in the Regulation of the Council of Ministers of 27 December 2022 on State aid granted to certain entrepreneurs for the implementation of new investments (Journal of Laws of 2025, item 108, as amended)..

According to the new regulations, the following enterprises are eligible for public aid in the form of tax exemptions:

- all enterprises in the sector of traditional industries, with the exception of enterprises producing, i.e.: explosives, alcohol, tobacco products, steel, or companies operating in the energy generation and distribution sector; wholesale and retail trade, facilities and construction works, services related to accommodation and catering services, and game centers. Companies from the metallurgy, iron and steel sectors, the coal sector, and the transport sector are not eligible for support under the EU’s regulations.

- selected enterprises from the business services sector (BSS) providing: IT services, research and development in the areas of natural and technical sciences, auditing and book keeping services, accounting (excluding tax declarations), technical research and analysis services, call centers, architectural and engineering services.

What is the amount of tax exemption?

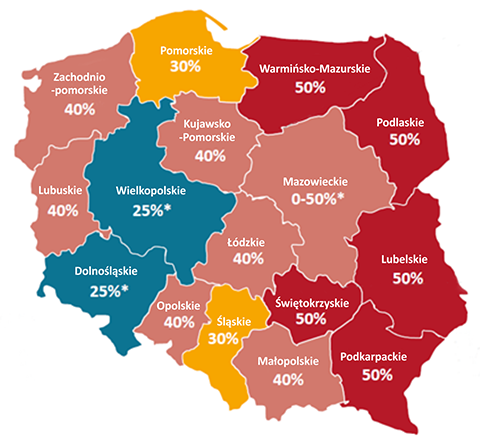

The maximum amount of state aid in the form of CIT or PIT tax exemption is determined on the basis of the regional aid map for 2022-2027 (representing the percentage of costs eligible for regional aid):

Regional state aid map 2022-2027

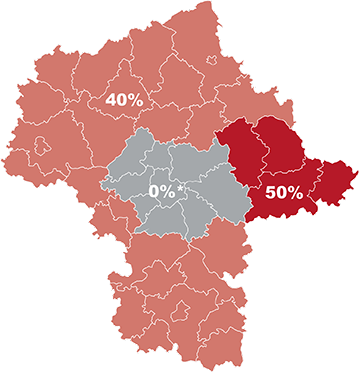

Mazowieckie region:

- 50% intensity: siedlecki subregion

- 0% intensity: Warsaw East and West subregion

- Exceptions for some municipalities:

- 25% intensity: Baranów, Błonie, Góra Kalwaria, Grodzisk Mazowiecki, Jaktorów, Kampinos, Leoncin, Leszno, Nasielsk, Prażmów, Tarczyn, Zakroczym i Żabia Wola;

- 35% intensity: Dąbrówka, Dobre, Jadów, Kałuszyn, Kołbiel, Latowicz, Mrozy, Osieck, Serock, Siennica, Sobienie-Jeziory, Strachówka i Tłuszcz.

Dolnośląskie region: Wrocław - 20% (from 2025 - 15%)

Wielkopolskie and Dolnośląskie regions are the so-called 'c' regions - a large entrepreneur can obtain aid only for an initial investment in favour of a new economic activity (i.e. not the same or a similar activity to the activity previously performed).

For micro and small enterprises: +20 pp

For medium-sized enterprises: +10 pp

For regions under the Just Transition Fund: +10 pp

What is more, PAIH operates a Generator of Investment Offers, in which you can check the conditions for obtaining tax exemption for a specific piece of real estate.

Support for medium and small/ micro enterprises is increased by 10 and 20 percentage points respectively (i.e. 25% becomes 35% or 45% respectively).

The exemption shall only be applicable to income generated from business activities carried out as part of an investment, covered by the decision on support. Therefore, if the entrepreneur simultaneously conducts activities which are not covered, the supported activities have to be organizationally separated and the level of exemption shall be determined on the basis of data (revenues and costs) of the separated activity. What is more, the Ministry of Finance has published explanatory notes on the method of determining tax-exempt income achieved from economic activity, as defined in the decision on support (referred to in the Act of 10 May 2018 on support for new investments), which clarified, inter alia, how to interpret situations when, because of the way in which a new and existing investment (located on the same site) are integrated, it is impossible to determine the income (revenue) exclusively from the new investment, without taking into account the integrated part of the existing investment (close links). The explanatory notes help to establish the best practice of applying the above-mentioned provisions, i.e. the most predictable, uniform and appropriate interpretation of the tax law.

In accordance with the regulations on state aid, the eligible costs of the new investment are:

- land acquisition cost, cost related to its purchase, the development or modernization of fixed assets (e.g. machines), cost related to the acquisition of intangible assets (computer programs, licenses, certificates, etc.), or

- 2-year labour costs of newly hired employees.

How to determine the company's status?

In accordance with the Commission’s Regulation (EU) No 651/2014 of 17 June 2014 declaring certain types of aid compatible with the internal market pursuant to Art. 107 and Art. 108 of the Treaty, the following evaluation criteria were adopted for the purposes of defining the size of enterprises: number of employees, turnover, balance sheet total, and independence. Turnover and balance sheet total are alternative criteria. On this basis, the following category of enterprises have been established:

- CategoryMedium

Small

Micro - Average annual

number of employed< 250

< 50

< 10and - Yearly

turnover≤ 50 EUR m

≤ 10 EUR m

≤ 2 EUR mor - Total annual

balance≤ 43 EUR m

≤ 10 EUR m

≤ 2 EUR m

Companies that do not qualify as micro, small or medium enterprise are classified as large companies.

Who decides on granting support?

The decision regarding support, issued at the entrepreneur's request, determines the period of its validity, the subject of economic activity, as well as the conditions that the entrepreneur has to meet. The decision is issued on behalf of the Minister responsible for the economy (currently the Minister of Economic Development), by the management of Special Economic Zones in the areas indicated in the ordinance to the Act.

A map of Poland with the areas administrated by Special Economic Zones separated

How long is the tax exemption granted for?

The period for which a decision on support is granted depends on the intensity of public aid for a given area. The time for utilizing public aid is the same for all companies, regardless of the type of business and the size of the company. The decision on support is issued for a specified period, not shorter than 12 years and not longer than 15 years. The period of exemption is calculated from the date of receiving the decision on support and is as follows:

- Decision

- Public aid intensity:

15%, 25%12 yearsDolnośląskie,

Wielkopolskie,

Warsaw Capital Region:

Baranów, Błonie, Góra Kalwaria, Grodzisk Mazowiecki, Jaktorów, Kampinos, Leoncin, Leszno, Nasielsk, Prażmów, Tarczyn, Zakroczym and Żabia Wola; Dąbrówka, Dobre, Jadów, Kałuszyn, Kołbiel, Latowicz, Mrozy, Osieck, Serock, Siennica, Sobienie-Jeziory, Strachówka and Tłuszcz - Public aid intensity:

30%, 40%14 yearsPomorskie,

Śląskie,

Kujawsko-Pomorskie,

Lubuskie,

Łódzkie,

Małopolskie,

Opolskie,

Zachodniopomorskie,

Mazowieckie regional region, except for the Siedlecki subregion - Public aid intensity:

50%

or for sites located in at least 51% within the boundaries of the SEZs15 yearsWarmińsko-Mazurskie,

Podlaskie,

Lubelskie,

Podkarpackie,

Świętokrzyskie,

Siedlecki subregion of the Mazowieckie

If, on the day the decision on support is issued, at least 51% of the area of land on which the new investment is to be located is situated within the boundaries of a special economic zone (as defined in Article 2 of the Act of 20 October 1994 on special economic zones), the decision on support for a new investment is issued for a period of 15 years.

What are the criteria for receiving public aid?

The decision on support is issued for the implementation of a new investment, which meets certain quantitative and qualitative criteria. The quantitative criteria (minimum amount of eligible costs) depends on the unemployment rate in the district (poviat) in which the investment is to be implemented (the higher the unemployment rate, the lower the required costs) and the size of the enterprise. Preference is also granted to entrepreneurs, conducting research and development activities and those in the business services sector.

Quantitative Criteria

Unemployment rate in the district/ average unemployment in Poland | Minimum amount of eligible costs | |||

Large enterprise | Medium enterprise | Small enterprise | Micro enterprise | |

<60% of national average | PLN 100 m | PLN 10 m | PLN 5 m | PLN 2 m |

60 - 100% | PLN 80 m | PLN 8 m | PLN 4 m | PLN 1.6 m |

100 - 130% | PLN 60 m | PLN 6 m | PLN 3 m | PLN 1.2 m |

130 - 160% | PLN 40 m | PLN 4 m | PLN 2 m | PLN 0.8 m |

160 - 200% | PLN 20 m | PLN 2 m | PLN 1 m | PLN 0.4 m |

200 - 250% | PLN 15 m | PLN 1.5 m | PLN 0.75 m | PLN 0.3 m |

> 250%* | PLN 10 m | PLN 1 m | PLN 0.5 m | PLN 0.2 m |

* and regardless of the unemployment rate - in 139 medium-sized cities losing socio-economic functions and in municipalities bordering these cities, as well as in the municipality where such a city is located, and in municipalities located within the following districts (poviats): augustowski, bartoszycki, bialski, białostocki, bieszczadzki, braniewski, chełmski, gołdapski, hajnowski, hrubieszowski, jarosławski, kętrzyński, lubaczowski, przemyski, sejneński, siemiatycki, sokólski, suwalski, tomaszowski, węgorzewski, włodawski, and in the city of Suwałki.

In the case of reinvestment in an existing plant (including the business services sector) planned by a large or medium-sized enterprise - the required eligible costs of the new investment are reduced by 50%.

Qualitative Criteria

SUSTAINABLE ECONOMIC DEVELOPMENT - max. 8 points | Points | ||

| MANUFACTURING SECTOR | BUSINESS SERVICES SECTOR |

|

Compliance with the current national development policy, where Poland may gain a competitive advantage | Investments in projects from the following sectors:

| 1 | |

R&D activity | Pursuing research and development activities | 1 | |

Professional activation | Professional activation through:

| 1 | |

Regional networking | Cooperation with suppliers, co-operators | 1 | |

Roboticisation and automation of processes | Purchase of an industrial robot | 1 | |

Green energy | Investment in renewable energy sources | 1 | |

Size of enterprise | Possessing the status of a micro, small or medium-sized enterprise | 1 | |

National Key Cluster | Membership of a National Key Cluster | Not applicable | 1 |

SUSTAINABLE SOCIAL DEVELOPMENT - max. 5 points | Points | ||

| MANUFACTURING SECTOR | BUSINESS SERVICES SECTOR |

|

Creating high quality jobs | Creating specialized jobs in order to pursue an economic activity covered by the new investment and offering secure employment | Creating well-paid jobs and offering secure employment | 1 |

Low negative environmental impact | Pursuing an economic activity with low negative environmental impact | 1 | |

Investment location | Locating the investment:

| 1 | |

Support in gaining additional education | Supporting the acquisition of knowledge and vocational qualifications and cooperating with vocational schools | 1 | |

Care for employees | Improving employees welfare | 1 | |

The entrepreneur implementing a new investment in a given sector shall be considered to have met the qualitative criteria once he obtains a certain number of points (depending on location - as indicated in the table below) no less than one point for each criterion:

Public aid intensity | Point threshold |

| 6 |

| 5 |

| 4 |